Another Bank Bites the Dust

by Gene Kirsch | October 5, 2011

On Friday, regulators closed First International Bank, Plano, Texas. This brings the total number of U.S. bank and thrift failures to 74 for 2011, behind last year’s pace of 127.

The southeast region accounts for nearly 50% of all bank failures for 2011. Across the country, Georgia leads the nation with 19 failures, Florida running a close second place with 11 bank closings, and Illinois is third with seven closings.

Because banks serve an important public purpose and are important to the nation’s economy, they are subject to intense regulatory scrutiny. Unfortunately the regulators don’t share their reviews and bank grades with the public. So, most times the public doesn’t hear about bank issues that may lead to failure until the bank is closed.

Luckily, the public does have another resource to keep on top of bank performance … Weiss Ratings.

Of the 74 institutions that failed in 2011, 72 or 97%, were rated E (“Very Weak”) by Weiss at the time of failure. Weiss rates 420 more banks and thrifts “Very Weak” with a rating of E+, E, or E-. You can view the full list at WeissRatings.com.

The Bank that Failed

First International was organized in 1991 as a state chartered

commercial bank. Before being closed on September 30, 2011, the

bank struggled in almost all areas of performance including

profitability, asset quality, regulatory capital and liqudity.

First International Bank, with assets of $239.9 million at June 30, 2011, had been rated “Very Weak” for the last five quarters by Weiss Ratings and was first identified as “Weak” in June 2008.

They reported a loss of more than $3.7 million for the period ended June 30, 2011. And, at the time of closing, they were not in compliance with FDIC Tier 1 (5%) and risk-based capital (6%) with ratios of 2.44% and 4.59%, respectively.

With non-performing loans representing a substantial portion, 25.4%, of their loan portfolio, it was clear the bank was in trouble. And increasing loss reserves only highlighted the expectation of further loan deterioration. Unfortunately, the bank’s investment in riskier commercial real estate and construction loans left them heavily exposed to sharp write-downs.

About Plano, TX

The closed bank was located in Plano, Texas which is actually one of the

prime places in the nation that continues to grow in both population and

business development. With strong household income (median income

$88,662) growing at 60% since 1990 according to HomeSight.com In

fact, Homesight data shows home prices still average $226,691 gaining

about 5% in value over the last 2-5 years.

Plano is located in the Dallas/Fort Worth area which was the fastest growing major market in the country in recent years, adding 1.3 million people between 2000 and 2009 according to the Census Bureau. The area’s growth was spurred by a favorable business climate: no corporate income tax, reasonable building costs and minimal regulations.

And, Plano continues to thrive as home to several Fortune 500 corporations including the 2 million square-foot corporate headquarters for JC Penney, a major clothing and houseware retailer. So, it would seem there’s more to the story when it comes to this particular bank failure.

When queried, a representative of the FDIC, LaJuan Williams-Young,

commented:

“First International Bank was a relatively small bank which experienced

losses associated with commercial real estate loans made to developers

including loans made in Nevada.”

American First National to Assume First International

American First National Bank, Houston, Texas, will assume the deposits

of First International Bank. They are a nationally chartered

commercial bank with assets of $708 million and a Weiss Rating of C-

(“Fair”). American First National specializes in commercial

lending and is a wholly-owned subsidiary of AFNB Holdings, Inc.

Before assuming the assets of First International, American First National had $5.3 million in year-to-date net income and a return on equity of 13.3% through June 30, 2011, about average performance for banks of their size. They also have more than adequate risk based capital of 15.36% and low non-performing loans of 2.26% compared to the industry average of 3.29%.

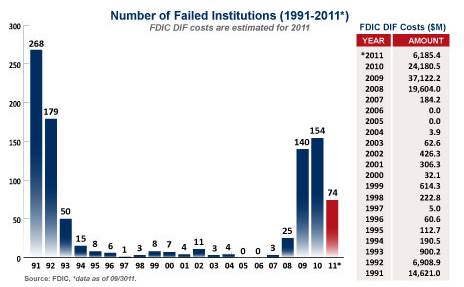

Bank Failure History

To date, bank failures in 2011 have been trailing 2010, not only by

count, but also in terms of lower impact on the Depositors Insurance

Fund (DIF). The FDIC maintains the DIF by assessing depositiory

institutions an inurance premium. The amount each institution is

assessed is based on the balance of insured deposits and the degree of

risk the institution poses to the insurance fund.

Bank failures typically represent a cost to the DIF because FDIC must liquidate assets that have declined substantially in value while at the same time making good on the institution’s deposit obligations.

Here’s some history to look at …

Gene Kirsch, senior financial analyst at Weiss Ratings, has more than 20 years of financial industry experience in credit-risk management, commercial lending and loan review analysis within various sized credit unions, finance companies and banks at both the retail and commercial level. He leads the firm's bank and thrift ratings division and developed the methodology for Weiss' credit union ratings.